Explainer: JD Logistics (2618 HK)

JDL: My Story Is A Lot Like Yours, Only More Interesting Cause It Involves Robots

Hi All!

Welcome to Post #1!🎉

This will be an Explainer post, where I lay out briefly what the company is all about. If the business is compelling enough, I’ll do a Deep Dive post where I really drill down into the details, build out an excel model and value the company. I will be writing about both public listed companies and pre-IPOs. Thank you and if you find it interesting and useful, do join the club!

Alright let’s go!

While going through the IPO docs of JD Logistics, the first thing that came to my mind was..Futurama. One of the funniest series on TV ever. Period.

Why Futurama? Cause its about delivery (well logistics to be straight), robots are a big part of the story and its big (like space geddit). The only thing that’s missing is pizza and robot devil.

JD Logistics went public end-May and was one of the more anticipated IPOs due to its relation to JD.com, a strong structural growth story and how it could disrupt a very very large industry that’s been too traditional for far too long.

Let’s see if this enthusiasm is warranted in 5 minutes or less:

What does it do? 👉 Business model

Drivers of growth 👉 Revenue

Risks👉 Roadblocks ahead?

Valuation 👉 Expensive?

Tea Leaves 👉 Final Verdict

1. Business Model

source: company filings

“We are the leading technology-driven supply chain solutions and logistics services provider in China. We offer a full spectrum of supply chain solutions and high-quality logistics services enabled by technology, ranging from warehousing to distribution, spanning across manufacturing to end-customers, covering regular and specialized items”

“Our value proposition is to empower our customers’ supply chains and substantially improve their operational efficiencies, which in turn enhance their own customer experience and stickiness. We help our customers reduce redundant distribution layers, improve the agility of their supply chains, and optimize inventory management”

As we so generously copy+pasted from the offering form here, JDL is Planet Express on steroids. They essentially handle a product from factory until its safely in the hands of the buyer and they do this in the fastest and most efficient way possible.

They do this for both their parent JD.com and more than 190,000 corporate customers across a range of industries from FMCG, apparel, 3Cs (computer, cons electronics, communication), automotive and even fresh produce. Maybe 🍕 isn’t too far off after all..

So how do they help customers?

Case Study: Study the case

How it helps:

According to channel checks (meaning asking/harassing the customers), the main benefit of a better logistics system is simple: It gets your products to the customers FASTER, which means it decreases the time your inventory is sitting in your warehouse UNSOLD which has all sorts of benefits like getting cash into your pocket faster, less warehousing needs etc

According to an automotive customer, using JDL’s intelligent warehousing service decreased overall inventory level by 15% which in turn resulted in faster inventory turnover. The system was able to intelligently place the spare parts in the most suitable located warehouse which is fantastic for a famously penny pinching industry.

For another customer in footwear, JDL’s systems managed to reduce fulfillment costs by 11% and delivery time by a whole 5 hours. As we will see later down the line, this is a key strength of JDL.

How it charges:

For corporate customers (bulk of customer base), JDL then signs master service agreements with their customers, charging them for the range of services rather than per service action. The lengths of these contracts are typically 1 year.

For individual customers which will typically use the normal express and freight delivery services, the pricing model is the typical per transaction basis (so thats the UPS/Fedex you and I are familiar with ie distance, weight and dimension of package).

2. Drivers (pun intended) of Growth

A) Large, no, GIGANTIC market

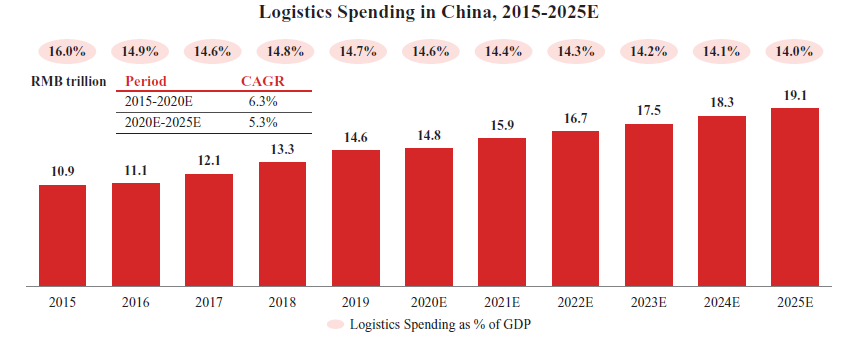

At RMB19.1 trillion (USD 2.9 trillion), China is ALREADY the largest logistics market in the world thanks to it being well..China.

source: company filings

But what caught my eye is that the segment JDL is in is growing even faster! While the overall industry is expected to grow ~5% a year from 2020-2025, the outsourced logistic service (aka 3P logistics) is expected to grow ~7% in the same period.

source: company filings

Why? Chinese companies are finding it harder and harder to handle the increasing volume and complexity in customer demand (eg same day delivery). On the other hand, 3P player’s infra and operational knowhow have evolved far more rapidly and are laser focused on providing best-in-class service. In other words, let the specialists do it! So in the future, its clear that JDL can have more of the pie as they sign up more customers in unpenetrated areas like Apparel, Pharma and Fresh Produce.

b) Robits

Bender may be a dick but he's rarely wrong. Any story that involves robots is probably going to be more awesome simply because robots are awesome.

Thats where JDL’s competitive edge lies - its technological advantage. The technology employed reads like a consultant’s book of buzzwords: 5G, AI, cloud, AMRs. As of December 31, 2020, JDL has >4,400 patents and computer software copyrights, of which over 2,500 relate to automation and unmanned technologies. JDL also has built a large team of >3,700 R&D point dexters, sorry, professionals.

“We leverage fundamental technologies such as 5G, AI, big data, cloud computing and IoT to continuously improve our capabilities in automation, digitalization, and intelligentization. We use advanced unmanned technologies and robotics, such as automated guided vehicles (AGVs), autonomous mobile robots (AMRs) and sorting robots, self-driving vehicles, among others…”

source: company filings

To emphasize their focus on technology, JD outspends their peers in R&D 7:1!!

And the crown jewel - JDL has the world’s first fully-unmanned storage facility, which was opened in Oct 2018. In addition to that, they operate 28 Asia No. 1 smart mega warehouses.

“JD.com opens automated warehouse that employs four people but fulfills 200,000 packages daily”

source: https://www.freightwaves.com/news/technology/jdcom-opens-automated-warehouse-that-employs-four-people-but-fulfills-200000-packages-daily

p.s in case you’re wondering who makes those little robots, its Hikvision (SHE: 002415) but that’s a story for another day.

c) Best in Service

Its a fact of life that customers are impatient. They don’t just want their products, they want it NOW. JDL is the ONLY e-commerce logistics company to attain same day delivery.

JDL can do this because it runs a fulfillment model (warehouses + last-mile parcel delivery), just like FBA (Fulfillment by Amazon). SF Express, the largest express delivery company in China by revenue, operates an end-to-end transportation logistics but have almost nothing when it comes to warehouse management. All this results in JDL getting some really happy customers.

3. Risks Roadblocks ahead(?)

A) Really fragmented market

China Logistics is a very very competitive and highly fragmented market. Even JDL, the market leader, only has a 2.7% share of the pie. The difference between JDL and player 2 may have widened from 1.2% in 2019 to 1.6% in 2020, yet its revenue is still low compared to global peers.

“According to the CIC Report, we are the largest player, in terms of total revenue, in China’s integrated supply chain logistics services industry with a market share of 2.7% in 2020.”

“The integrated supply chain logistics services market in China is highly fragmented due to the vast size of the market and specific requirements across industry verticals.”

“The top ten players only accounted for 9.0% market share in terms of revenue in 2020”

JDL’s cheerleaders say JDL is the next FBA. But the logistics environment in the US is very different from that of China. In the US, the competitive landscape is FAR lower with only 2-3 major players with price on a gentle upward trend at 5% increase per year. In China, logistic pricing is challenging and has gone DOWN by ~10% each year in the last decade. So fulfillment cost per order rises slowly for Amazon (without causing much issue) but for JDL this is a major issue or JD Group will be less competitive.

Competition has also been heating up. SF, JDL’s biggest rival in e-commerce logistics, recently acquired Kerry Logistics (and previous DHL's supply chain business in China). By consolidating Kerry Logistics into the combined entity, SF will significantly expand its SCL capability, particularly in Asia markets.

B) Scale first, Profits later

Despite the fancy story, JDL has never made a profit in its 14 years of operations. In the last reported 3 years it has seen its losses increase from RMB2.7bn (~USD418 mn) to RMB4.0bn (~USD619 mn) despite almost 2X-ing its revenue.

source: company filings

And don’t expect it this to change for the next few years at least. If you thought losing USD619 mn in 2020 was bad, wait till you read the part in the IPO prospectus where management expects losses to further widen in 2021.

Where is all this money going to? Scale expansion.

Expanding scale is the only way to bring down unit logistic cost. As growth from the c

ore JD platform inevitably slows, the next stage of growth for JDL will have to come from its external customers beyond the e-commerce space in supply chain logistics, which as mentioned before, is hyper fragmented with a large number of low tech labor-intensive operators. This will mean lowering prices + even more sales and marketing efforts = pressure on profitability for the foreseeable future. Safe to say, Buffett will be giving this a miss.

4. Valuations

JDL is by no means a bargain bin find. With it being loss making the moment you cross the GP line, it doesn’t leave one with much choice but to compare it on a top line basis. Chinese ADRs have also been seeing a selloff (at time of writing) which is reducing appetite for loss making Chinese companies.

source: Koyfin

Looking at closest comparable peer SF Express isn’t much help. Valuation has come down by 40% YTD after a surprise statement from SF forecasting a quarterly loss.

JDL also didn’t see that much of an IPO pop suggesting that investors are still adopting a wait and see approach. At least it didn’t fall 16% like SF Reit did on its IPO just 10 days before.

5. Final Verdict

Final verdict: NOT CONVINCED.

Despite the exciting story and monster revenue growth, 3 things are putting me off:

1) Industry is too competitive and looks to stay that way. Too much competition keeps a lid on pricing power and leaves companies no choice but to grow by increasing volume. This brings us to..

2) JDL will have to keep re-investing to build scale to stay ahead of the competition. JDL might be asset light on the surface but that’s cause JD is footing the bill of building out warehouses at this point.

3) I can’t see a path to profitability in the next few years. And to sleep at night I need my companies to generate at least some profit.

The hunt for the next high conviction idea continues.

-Core Convictions

P.S please do post your thoughts in the comments!